The role of information technology in improving auditing quality and reporting at the State Audit Bureau of Kuwait

Data is considered the new black oil relying upon traditional auditing won’t lead to accurate results especially when auditing complex transactions. Traditional audits lack accuracy and therefore impact the quality of audits. Audit software aid auditors in complex audits, they help enhance the quality of work, the working environment and save time. This research will focus on the importance of information technology in audits and how it has a direct impact on quality in all auditing phases including documentation and reporting.

Research question:

- Does the State Audit Bureau of Kuwait have a clear methodology to audit accounting information systems in entities subject to their oversight?

- How does the use of information technology impact audit quality and how is it reflected in reporting?

Text of the paper/article:

The audit profession nowadays faces many challenges especially when it comes to the need for computer-aided audits as a result of massive data volume which needs to be audited in today’s complex business environment. Data is considered the new black oil relying upon traditional auditing won’t lead to accurate results especially since most of today’s data is digitalized. Traditional audits make auditors face challenges like missing deadlines resulting in a lack of submitting tasks on time, this led to developing multiple audit software’s to avoid challenges caused by traditional audits (AlThunayan, 2017; Fotoh, 2020).

Lack of information technology in audits resulted in many problems. Auditors today are required to keep pace with information technology by enhancing the audit environment and audit clients (AlThunayan, 2017; Bradford et al., 2020). Clients today are required to change the way they work including storing information and documenting audits (AlThunayan, 2017; Bradford et al., 2020; Fotoh, 2020). A traditional paper environment today is not feasible, changing the way data is stored and moving towards a paperless environment should be the goal of most clients especially when it comes to audit documentation. Paperless environments led to the development of reliable systems and software’s in which all stages of auditing are involved (Vuori et al., 2018).

The rise of many audit issues and challenges made us focus on researching a problem that focuses on the relationship between information technology and improving the quality of audits in the State Audit Bureau of Kuwait.

This research will focus on studying information technology requirements in auditing at the State Audit Bureau of Kuwait and their importance in enhancing and improving audit quality and the impact it has on reporting.

The focus of the research is to shed light on the requirements needed to apply information technology in audits performed by the State Audit Bureau of Kuwait and the use of information technology in raising the quality of audits in addition to its reflection on the reports issued by the State Audit Bureau of Kuwait. This research will also focus on the development of auditor’s skills by developing a framework that helps auditing using information technology.

Introduction

The business environment in the last two decades witnessed drastic changes and challenges, the most important of which are related to information technology and digitalization. This resulted in significant changes also in the auditing profession it led to the development of accounting systems and applications which contribute to raising audit quality and enhancing reporting (Van der Nest et al., 2017; Vuori et al., 2018). Many supreme audit institutions today focus on digitalization and developing a paperless environment as it contributed to improving and enhancing audits and the reporting process. Technology also helps overcome challenges and obstacles that auditors face in a traditional setting (Coman et al., 2018; INTOSAI, 2019; Knechel, 2016).

The State Audit Bureau of Kuwait has an important role in contributing to the achievement of effective oversight. Achieving the State Audit Bureau mission with high quality and expertise requires the development of a framework that focuses on information systems and technology. The state audit bureau has a system named “Audit Management System” it represents a qualitative leap in linking the audit teams with various entities (State Audit Bureau, 2017). However, the system still lacks some essential success factors and many users face issues when using the system. This research focuses on a problem that is not yet solved in the State Audit Bureau which is how information technology helps in raising audit quality, it will also focus on the development of auditor’s skills related to the use of information technology.

This research article will also discuss some conclusions and recommendations on how to enhance reporting by improving the quality of audits through the use of information technology.

Research problem

The State Audit Bureau lacks in providing minimum information technology requirements in conducted audits, this will have a great impact on the quality of performed audits and reporting. In addition, it harms improving and developing audits conducted by the State Audit Bureau of Kuwait.

Research Question

Major research questions:

- Does the State Audit Bureau of Kuwait have a clear methodology to audit accounting information systems in entities subject to their oversight?

- How does the use of information technology impact audit quality and how is it reflected in reporting?

Hypothesis one: There are no minimum requirements for information technology application in the State Audit Bureau of Kuwait.

Hypothesis two: There are no benefits and obstacles in using information technology to perform and document audit work.

Hypothesis three: Absence of information systems audit methodology in State Audit Bureau of Kuwait

Research importance

The State Audit Bureau is working continuously to keep pace with new auditing and accounting trends related to the development of institutional performance. This helped the State Audit Bureau achieve excellence in performance fulfilling its responsibilities with the highest levels of professionalism and independence. Continuous development enhances the State Audit Bureau's role in addition to improving work through the use of modern information technology.

The importance of the research falls in having a clear audit methodology for information system audits and the importance of information technology in improving the quality of conducted audits. In addition, to how quality is reflected in reporting phase in the State Audit Bureau. The research will also show a glimpse of the advantages and disadvantages of using information technology during all audit phases including documentation.

Research objectives

- Understand the concept of information technology.

- Identify the requirements for applying information technology in audits performed by the State Audit Bureau.

- Identify the advantages and disadvantages of using information technology in audits.

- Understand the current method of auditing information systems at the State Audit Bureau.

- Identify how information technology improves quality and how this is reflected in State Audit Bureau reports.

Research methodology

A field study was conducted using a questionnaire, results of the field study that we carried out to measure the role of information technology in improving the quality of audits and how skillful employees are when it comes to information system audits.

The researcher designed a questionnaire directed to workers in multiple sectors at the State Audit Bureau of Kuwait including the oil sector, companies, investment, performance control unit, ministries, and information technology. The questionnaire was distributed to the following job titles: assistant auditor, associate auditor, auditor, senior auditor, main auditor, chief auditor, and experts. The questionnaire aimed to answer the two main research questions and this was done through (18) questions.

The questionnaire included 18 questions that were evaluated and measured using the Likert scale, where “1” fully agreed, “2” agree, “3” neutral, “4” do not agree, “5” completely disagree. In addition, to some job designation-related questions to determine the characteristics of the person who gave the opinion and to be able to know which sector has more skills when it comes to information technology than the other. Results were then fed into a statistical software SPSS for analysis.

Questionnaires were distributed manually to all sectors concerned with the research topic. (91) questionnaires were collected from a total of (100) distributed questionnaires as (9) questionnaires were not filled in, with a response rate of 91% from the total number of distributed questionnaires.

Research results

Results were analyzed using the statistical software SPSS and findings were as follows:

Results were analyzed using the statistical software SPSS and findings were as follows:

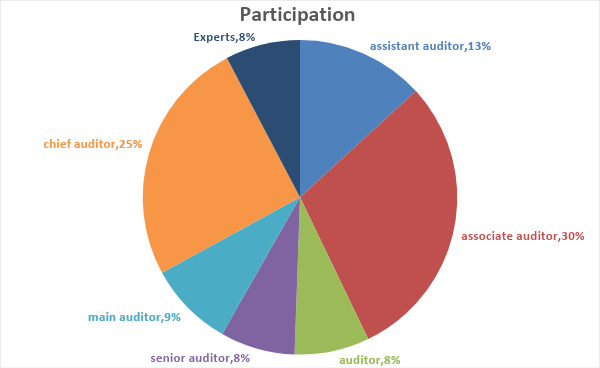

- 29% of participants were associate auditors as shown in figure 1 below:

Figure 1

Pie chart showing the percentages of participants based on their job title

- 52.7% of respondents lack skills when it comes to auditing using information technology, this represents an extremely high percentage more than half of the sample lack skills and knowledge in audit software

- 60.4% of respondents never used auditing software as shown in figure 2 below:

Figure 2

SPSS results for the question: Have you used auditing software in your previous audits?

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

||

|

Valid |

yes |

36 |

39.6 |

39.6 |

39.6 |

|

No |

55 |

60.4 |

60.4 |

100.0 |

|

|

Total |

91 |

100.0 |

100.0 |

- 85.7% of respondents prefer the use of information technology in audits, this shows that they believe the advantages outweigh the disadvantages.

- 54.9% of the respondents have read about the use of information technology in the State Audit Bureau general manual.

- 95.6% of the respondents agreed that the use of information technology in audits will improve the overall reporting quality as shown in figure 3 below:

Figure 3

SPSS results for the question: Does the use of information technology in audits improve quality?

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

||

|

Valid |

yes |

87 |

95.6 |

95.6 |

95.6 |

|

no |

4 |

4.4 |

4.4 |

100.0 |

|

|

Total |

91 |

100.0 |

100.0 |

- 78% of the respondents agreed that the State Audit Bureau does not have a clear framework and manual for the use of information technology in audits.

- 90% of the respondents agreed that reports issued using audit software are more accurate and detailed.

- 84.6% of the respondents see that information technology advantage outweighs its disadvantages as seen in figure 4 below:

Figure 4

SPSS results for the question: Advantages of information technology in audits outweigh the disadvantages.

|

Frequency |

Percent |

Valid Percent |

Cumulative Percent |

||

|

Valid |

Completely agree |

31 |

34.1 |

34.1 |

34.1 |

|

Agree |

46 |

50.5 |

50.5 |

84.6 |

|

|

Neutral |

12 |

13.2 |

13.2 |

97.8 |

|

|

Disagree |

2 |

2.2 |

2.2 |

100.0 |

|

|

Total |

91 |

100.0 |

100.0 |

||

Research recommendations

- Create awareness campaigns on the use of information technology in audits.

- Conduct workshops that train auditors using real-life examples on how to audit using audit software.

- Study and learn from other supreme audit institutions' experience in information system audits and auditing software.

- Share peer reviews and experiences with State Audit Bureau employees via email or training courses.

- The State Audit Bureau has to offer auditing software or multiple software’s to help employees apply what they learn in training courses and improve the quality of audits which will be reflected in reporting.

- Motivate employees on the use of information technology as digitalization is the future.

- Start to digitalize the State Audit Bureau reporting process, small steps will lead to a better-digitalized environment in the future.

- Develop an audit methodology that supports information system audits.

- Develop a framework that will help auditors in auditing using information systems through all audit phases.

Conclusion

Digitalization is part of life in today’s working environment, the use of information technology is a must for success. Auditing requires the use of information systems and technology. Audit software has many advantages that reduce work stress on employees that have to audit a huge amount of data, advantages of information technology use are reflected in the quality of work and audit through all phases especially in documentation and reporting.

Author: Fatimah Nabil

Bibliography:

AlThunayan, A. (2017). Basics of auditing on information systems. State Audit Bureau. https://www.sabq8.org/sabweb/Files/SABMagazinePublishedIssue/%D8%A7%D9%84%D8%B9%D8%AF%D8%AF%20%D8%A7%D9%84%D8%B1%D8%A7%D8%A8%D8%B9%20%D9%88%D8%A7%D9%84%D8%AE%D9%85%D8%B3%D9%88%D9%86/files/assets/common/downloads/publication.pdf

Bradford, M., Henderson, D., Baxter, R. J., & Navarro, P. (2020). Using generalized audit software to detect material misstatements, control deficiencies, and fraud. Managerial Auditing Journal, 35(4), 521–547. https://doi.org/10.1108/maj-05-2019-2277

Coman, D. M., Coman, M. D., & Munteanu, C. C. (2018). Integrate CAATS Technologies into Data Selection and Data Analysis. Valahian Journal of Economic Studies, 9(1), 29–38. https://doi.org/10.2478/vjes-2018-0003

Fotoh, L. E. (2020). Critical issues of the audit expectation gap in the era of audit digitalization. HARC, 2020. https://scholarspace.manoa.hawaii.edu/bitstream/10125/70482/HARC-2021_paper_64.pdf

INTOSAI. (2019). Guidance on audit of information systems. https://www.issai.org/wp-content/uploads/2019/09/Guid-5100-Guidance-on-Audit-of-Information-Systems.pdf

Knechel, W. R. (2016). Audit Quality and Regulation. International Journal of Auditing, 20(3), 215–223. https://doi.org/10.1111/ijau.12077

State Audit Bureau. (2017). General audit manual. http://www.sabq8.org/sabweb/pages/Reports/SpecialForAuditor.aspx

van der Nest, D. P., Smidt, L., & Lubbe, D. (2017). The use of generalized audit software by internal audit functions in a developing country: A maturity level assessment. Risk Governance and Control: Financial Markets and Institutions, 7(4–2), 189–202. https://doi.org/10.22495/rgc7i4c2art2

Vuori, V., Helander, N., & Okkonen, J. (2018). Digitalization in knowledge work: the dream of enhanced performance. Cognition, Technology & Work, 21(2), 237–252. https://doi.org/10.1007/s10111-018-0501-3