Price strategy challenges of Ethiopian coffee exporters

This paper accesses the Ethiopian coffee export trade policy’s challenges in the field of pricing strategy. The situation is analyzed and accessed with the help of a survey consisting of an interview, questionnaire survey and document analysis. The main problems of pricing strategy are analyzed and at the end, the recommendations are given. The paper is a part of a larger study and therefore its limitation are that it is not exhaustive in terms of data sources and variables of analysis. The paper is believed to benefit those stakeholders in the export sector to see their weaknesses and strengths.

INTRODUCTION

In this article, we deal with the Ethiopian coffee exporter policy challenges in the pricing strategy. The article is a part of a larger study and is concerned with one of four (event. five) dimensions of marketing communication: price, place, promotion and product. A competitive price and effective marketing communication based on marketing strategy help companies to achieve its targets. The marketing strategy should reflect these dimensions or elements as inseparable because each affect the other. In our case, the company offers the customers commercial coffee only. The company also starts to export specialty coffee; this is important in effectively using 4Ps of the marketing mix. We need to consider coffee accessibility and availability as well. That means, to have a suitable warehouses and processing unit, which have a good potential to export coffee at available time.

In terms of pricing strategy, the company sets an affordable price and easily understandable by its customer. The coffee price is set upon the customer’s perceived value, cost, and benchmarking of some exporter´s price. Hence it couldn´t consider only the competitor analysis in order to set the pricing strategy.

Regarding the competition, there are many coffee exporters in the industry, but the business component doesn´t have a designed strategy to win the competition and companies are doing business based on previous goodwill of the company. The quality of the export coffee satisfies its customers. The pricing strategy of the business unit is very complicated because of the business nature, but it is understandable to the customer. The business unit considers cost, perceived value, and product value as a benchmark in setting the price strategy. Sometimes the strategic marketing documents show that the company did not correctly state what factor was considered in setting the pricing strategy.

Coffee policy in Ethiopia

The Ethiopian government’s coffee policy is concerned with trade and control of the hard currency earned from exports to maximize foreign exchange. There are no policies affecting coffee production. There are some regulations affecting the marketing process: it is illegal to sell export quality coffee on the local market even if there is a better local price. Any coffee-related business requires a special license for domestic wholesaling, coffee exporting, or coffee roasting. In May 2011, the Ethiopian government introduced a coffee storing and exporting regulation limiting the amount of stock that an exporter can store. Any exporter storing more than 500 tons of coffee without having a shipment contract with an importer will be penalized by revoking the trader’s right to buy or sell coffee at the Ethiopian Commodities Exchange (ECX) for three months. Ethiopia commodity Exchange (ECX) was established to handle the marketing of agricultural commodities like coffee, sesame, and beans. Nearly all coffee is sold on the ECX floor either directly through an organized coffee producer’s cooperatives, or intermediaries. ECX is a public market, facilitating institution that was established in 2008 with the help of United States Agency for International Development (USAID). ECX’s board members are government officials, providing them an opportunity to have a regulatory hand in the coffee marketing process. The main reason for establishing ECX was to eliminate the vast number of intermediaries involved in the coffee distribution and enable coffee farmers to benefit from prevailing market prices. Coffee sold through ECX is considered commodity coffee and will not get the possible premiums organic coffee. Ethiopia mainly exports green beans with only a minimal amount of roasted beans. Ethiopian coffee is currently 70-80% unwashed or sun-dried, and 20-30% washed coffee. Unwashed coffee commands a lower price in many markets, including the US. The image of washed coffee being somehow “cleaner” is vital in the US. Some countries specifically require unwashed coffee for its better and richer taste, especially in the Japanese market. Coffee grading is conducted by ECX using a well-established laboratory. Grading is conducted by analyzing two aspects of the coffee bean: First, the raw green beans are visually evaluated for defects, and the second ECX uses taste testers to identify sensory aspects of a roasted bean, including the aroma, taste, acidity, and other flavors. The ECX bidding system is an “Open Cry Out” system where sellers and buyers meet on an open trading floor to negotiate and finalize the sales deals.

Methodology

The author of this paper has conducted his own research using questionnaires, interviews with selected experts and document review. Interviews were conducted with key informants selected from three institutions among the eight sample organizations. The research used a non-probability sampling technique, specifically judgmental sampling. Five respondents were selected from each organization on a judgmental basis. The research covered interviews with three executives (one from the Ethiopian Chamber of Commerce and Sectorial Associations, one from Nedhi coffee Exporters PLC., and one from the Ministry of Trade and Industry). These respondents were selected for an interview since they were more competent with issues relevant to the research. The interviews provided information useful to identify strengths and weaknesses of the Ethiopian coffee export policy, challenges of getting access to the international market for Ethiopian products, and the strengths and weaknesses of the parties involved in export processing.

Another method of research was a document review. Documents were collected from the Central Statistics Authority (CSA) of Ethiopia, the Ethiopian Customs Authority (ECuA), the National Bank of Ethiopia (NBE), the Ministry of Trade and Industry (MoTI), and the Ethiopian Economic Association (EEA). The reviewed documents comprise Trade Data Monitor (TDM) annual Reports on export trade during the years 2017/18 until 2018/19, reports of the Central Statistics Authority of Ethiopia, data from the Ethiopian Customs Authority, data from the Ministry of Trade and Industry, and the Ethiopian Economic Association’s 2019 /20 quarterly report. The annual reports of NBE provided the changes in the overall balance of payments for the consecutive years under consideration. These documents also provided information on the trade balances, developments in Ethiopian merchandise trade, price changes of the major export items, the volume of major export items, revenues of the major export items, the export share of selected items, and exports of primary commodities destination.

The survey questionnaire consisted of a variety of questions, including both close-ended and open-ended ones. Questionnaires were returned by 140 respondents. The respondents reflected their opinions on a variety of issues concerning the Ethiopian coffee export policy challenges.

For instance, the respondents gave their opinions on the competitiveness of the challenging policy of the Ethiopian coffee export sector products regarding quality, reliability, and cost-effectiveness. The respondents also reflected the Ethiopian coffee exporters’ capacity. These opinions cover the state of backward and forward linkage of Ethiopian coffee exporters, industry problems of policy like structure, management capacity, market knowledge, the state of skilled human resources in the sector, and the export sector’s integration. Furthermore, the respondents’ opinions cover the effectiveness of facilitation support and services in the Ethiopian coffee export sector. The respondents also provided assessments on various policies’ conduciveness to assist the private sector accessing international markets. These opinions address infrastructural, institutions, and informational supports provided by such parties as to the chambers of commerce, export promotion agencies, regional economic integration, and export market research institutions.

Research data

According to some respondents, the Ethiopian Coffee harvest is still low in Ethiopia. This low productivity is often caused by a disease, such as coffee berry disease (CBD). In particular, CBD has been causing severe crop losses, accompanied by inadequate and traditional management practices and a shortage of improved and adaptable coffee seed varieties.

Low returns for farmers due to low prices mean lowering the agricultural household income, agricultural wages, and loss of employment. Farmers are the ones most affected by international agricultural products price movements. A reduction in their earnings creates a vicious circle of challenges. It is challenging to mobilize investment resources to improve production, especially in introducing environmentally‐friendly production methods. This leads to inactivity in productivity, competitiveness and shortage of incomes. Farmers are often unable to use improved seed varieties or adopt scientific and technical advances (improved technologies). The result is poor crop management and low yields. This situation threatens the country’s coffee economy’s sustainability, heavily dependent on coffee. Quality inconsistency and deterioration are often due to some natural calamities, such as drought, irregular rainfall, and improper processing. This is the case of areas where the unwashed/sun-dried coffee processing method is predominantly practised. In the situation of ever-increasing coffee prices, domestic suppliers do not get sufficient access to loans. Coffee producers require large sums of money early in the season to purchase input supplies and hire labor. In Ethiopia, regulatory constraints, such as strict lending policies and government-mandated collateral requirements, make it nearly impossible for smallholder farmers to obtain financial support without a loan guarantee. This lack of access to capital made it very complicated for smallholders´ coffee producers. Most of them have limited records of accomplishment where no formal collateral is practiced.

Many wet mills in the country could buy cherry coffee from farmers and sell green coffee a few months later without any protection from a fall in the international market price. While producers of specialty-grade coffee are typically less prone to the international volatile price shocks, the market’s unpredictable boom-and-bust nature remains a challenge for all suppliers. Hence, the non-existence of price risk management is one of the challenges that persist in the coffee export sector.

The research data show that Ethiopia coffee export has adopted several pricing strategies; there is a significant positive correlation between Ethiopia coffee export sector profitability of Ethiopia coffee export and pricing strategy. The research also concluded that adopting a pricing strategy has a significant positive effect on Ethiopia coffee export sector’s profitability. As observed from the research data, customers have repeatedly reported that the price set for this disposable sanitary product is high and challenging for the lower class of the population to afford it.

Ethiopia is one of the largest coffee exporters in Africa. Coffee represents between twenty-seven and thirty-one percent of the country’s commodity exports averaged over the last four years. International buyers value Ethiopia’s Arabica coffee for its unique, smooth taste. Ninety-five percent of the country’s coffee is cultivated by 4.5 million farming households.

In Table 1 below, we can see the comparison of the top 10 countries producing green coffee between the years 2017 and 2019. We can conclude that Ethiopia has raised its production and the trend continues with 7450 in 1000 60 kg bags in 2020.

| NO | Country | Production in 2017 | Production in 2018 | Production in 2019 |

| 1 | Brazil | 56100 | 52100 | 66500 |

| 2 | Vietnam | 26700 | 29300 | 30400 |

| 3 | Colombia | 14600 | 13825 | 13870 |

| 4 | Indonesia | 10600 | 10400 | 10600 |

| 5 | Ethiopia | 6943 | 7055 | 7350 |

| 6 | Honduras | 7515 | 7600 | 7510 |

| 7 | India | 5200 | 5266 | 5325 |

| 8 | Uganda | 5200 | 4350 | 4800 |

| 9 | Peru | 4480 | 4375 | 4225 |

| 10 | Mexico | 3300 | 4000 | 3550 |

Table 1. Green Coffee Production by Country in 1000 60 KG BAGS in 2017, 2018 and 2019 (source: Index Mundi, 2021)

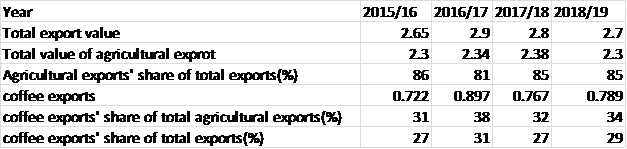

In the following Table 2, we can see the export value of Ethiopian coffee and partial shares in agricultural production in the years 2015 to 2019. We can see that coffee export share in the total agricultural export has declined between the years 2016 and 2018, but in the following year in rose again. The share of coffee on total export has also risen between the years 2018 and 2019, the value of agricultural export remains the same.

Table 2. Value of Ethiopia coffee as a share of the total – in billion (source: Post calculation based on the data from Ethiopia Revenue and Custom Authority)

In the administered interviews there were two questions directly aiming at pricing strategy, specifically on those elements of marketing strategy that can company use to compete within prices of goods. The first question asked how the company plan to combat the competitors who export a product that is cheaper. The respondents stated that in the current situation Ethiopian coffee exporter is not contesting anyone because there is no company export of the inequality products. “The aim of the exporter is exporting product’s quality is not compromised, and there is no significant price change. In that case, there is no reason for our customers to jump shift from our product since the product we provide is seen as a necessity,” stated the respondent. That means, currently the product is so unique that almost has no competitors in the (local) filed. The second question asked on the marketing strategy challenges faced by the organization and the means to counter-attack those challenges. The respondent stated that the big issue for the organization is using strategies that are not crafted by utilizing any pilot study or market survey. Furthermore, the respondents admitted that: “In order to beat the probabilities, there should be a pre-planning and marketing survey.” Another challenge for the organization is the situation and customs in global market demands in the sense that there is a lower price rate for products that are sold in the global market and distribution is given to exporter so that moving the product out of the warehouse can take a long time.

As the answers indicate, the company believed that this should improve service quality depending on customer response by providing quality products, improving the quality, delivery, and focusing on cost reduction to compete with others. The respond regarding the pricing strategy of the company stated no treat in adverse interest as far as the objective is given, generating market openings to the producer is concerned, all pricing element for its cost-build up is included, comparison with the free market is done and then the competing environments are analyzed, and especially considered is the factor that includes the cost of the product, customer demand of the product, profit of the product, distribution objective, and strategies as quality distribution, decreases costs, increases speediness and more market covered. Additionally, the respondent believed that customers recognize their pricing strategy; it is an indication for the competition to think about what is there outstanding when our company is out of the market for some reasonable time.

In the following Table 3, we can see answers from the questionnaire regarding pricing challenges of Ethiopian exported coffee.

The results show that the Ethiopian coffee product exports prices are challenging (Mean = 3.7357), so that the results are implying that the price challenging for competitors on the global market, as shown by item no. 2 (Mean = 2.176). The price of Ethiopian coffee has a tremendous challenge to competitors over the world market. As the results of item no. 3 show, the majority of the respondents strongly disagree that Ethiopia coffee products discount the prices because of the lack of quality (Mean = 2.150). It implies that Ethiopian coffee products have excellent quality, but there are more competitors on the global market and there is a lack of volume exports and also there is limited export in the destination area of the country. The results of item no. 4 indicate a challenge to get an actual price from a coffee exporter (Mean = 3,8857); most respondents strongly agree with the statement and it implies that the exporters have to keep their own secret and no selling information between each other. The results of item no. 5 indicated that Ethiopian coffee product price is increasing in the global market (Mean = 3.5143); it implies that the price of Ethiopian coffee is not increasing in the global market. According to some respondents, the volume of Ethiopian coffee exports has been increasing due to covid-19 because many people were sitting at home and increasing coffee consumption. Results of item no. 6 show that the higher price is affecting coffee exporter (Mean = 3.5643), the majority of respondents agreed on that that the higher price of the coffee has been decreasing the volume of exporting of the products and also impacting the coffee exporter, discouraging exporter business of the country. In question no. 7 respondents answered the question about the price of Ethiopian export coffee. Most of the respondents (Mean = 1,8629) disagreed with the statement and they see the price of Ethiopian export coffee as unsatisfying. The results of item no. 8 indicate that customers were satisfied with the current overall pricing system of Ethiopia coffee (Mean = 2.2357). The results of item no. 9 show that respondents agree (Mean = 3.5357) on that the major challenge of Ethiopian coffee exporter´s is the absence of competitor prices analysis. The results of item no. 10 indicate that attracting a new buyer and increasing the quantity of the export product decreases selling prices (Mean = 3.7357); the majority of respondents strongly agree with that when new customers come to the business, the exporter encourages the first period to enter with decreasing the selling price until adapting to the market and also increasing the volume quantity of export. The results of item no. 11 indicate that most respondents agree (Mean = 3.7857) that the decreasing price of coffee has an impact on the exporter of profit.

| No | Items | Mean | Standard deviation |

| 1 | Ethiopian coffee product exports prices are challenging | 3.7357 | 1.24433 |

| 2 | There is a price challenging with other competitors | 2.1786 | 1.27097 |

| 3 | Ethiopia coffee product discounts prices because of lack of quality | 2.1786 | 1.22870 |

| 4 | There is a challenge to get an actual price from coffee export | 3.8857 | 1.34156 |

| 5 | Ethiopian coffee product prices are increasing in the global market | 3.5143 | 1.36496 |

| 6 | Are the higher price affecting coffee exporter? | 3.5643 | 1.3376 |

| 7 | Is the price of the Ethiopian export coffee good? | 1,8629 | 1.03376 |

| 8 | It satisfies customers with the current overall pricing system of Ethiopia | 2.2357 | 1.26724 |

| 9 | The major challenge of Ethiopian coffee exporter is no check of competitor prices | 3.5357 | 1.47112 |

| 10 | Attracting a new buyer and increasing the quantity of export product decrease selling prices | 3.7357 | 1.22098 |

| 11 | The decreasing price of coffee has an impact on the exporter in profit | 3.7857 | 1.07145 |

Table 3. Pricing challenges (source: survey data 2020)

The results of Table 4 show the respondent´s opinions on the pricing policy’s objectives. Most of the respondent mentioned maximizing profit – 77 respondents from 140 (55.0%). Penetration of the market was mentioned by 40 respondents (26,6%) and discouraging the competitor was mentioned by 23 respondents (16.4%). The results show that the Ethiopian coffee exporter is more considering maximizing the profit of the own company than the market penetration of the products, which is not suitable for product development. Market share growth shows that it is challenging for product development and exporters need to aware of market penetration and product development.

| In your view, what are the objectives of your pricing policy? | Maximizing profit77(55%) | Penetration of market40(28,6%) | Discouraging competitor23(16.4%) | 0 | 1.7357 | .87828 |

Table 3. Pricing policy objectives (source: survey data 2020)

From the findings, we can conclude that Ethiopian coffee export prices mainly depend on the external market. This is out of the control of the exporters. It is severely affected by the exporters’ competitiveness – the price offered by ECX sometimes much more than the international price. Thus, exporters face the problem of meeting commitments as per their sales contract. Lack of professional advice at the time of Letter of Credit and document negotiation is also considered a problem in price reduction and rarely shipment rejection by the buyers.

Lack of integration among all concerned parties negatively affected the transaction flow of the sector.

Conclusion and discussion

Ethiopia is one of the essential coffee producers. The export has mostly been due to increases in international market prices. Quality improved only slightly over time, but the quantity exported increased from time to time, seemingly explained by increased domestic supplies as well as reduced local consumption. To further improve export performance, investments to increase the quantities produced and improve quality are needed, including an increase in washing, certification, and traceability.

Coffee is one of the most essential traded commodities in the world. The sector’s trade structure and performance have extensive development and poverty implications, given small-holders’ high production concentration in poor developing countries. Coffee’s global value chains are quickly transforming because of shifts in demands and an increasing emphasis on product differentiation in importing countries (Ponte 2002; Daviron and Ponte 2005). There is a growing willingness-to-pay for premium, high-quality coffee by affluent consumers. The demand for specialty and certified coffee is on the rise. Moreover, international coffee markets have experienced significant price variation over the last decade – prices were five times higher in 2011 than in 2002.

These changes have important implications for many of the poorest developing countries, as most coffee production occurs in these countries, even though most coffee consumption is in developed countries (Pendergrast, 2010; Ponte, 2002). While some studies have looked at price formation for different types of coffee at the retail consumption level in importing countries (e.g., Teuber and Herrmann, 2012), important questions remain on who benefits from this increasing willingness-to-pay for coffee and on how changes in global coffee markets are transmitted to producing countries. Moreover, few researchers have looked at how domestic policy change affects the coffee sector exporting countries.

Over the last decade, we also note a large increase in the value of coffee exports over time. This change has mostly been driven by increases in international prices and, to a lesser degree, by the increased quantity and quality of export. While the exported quantity has increased, this has seemingly been driven by both increased production and reduced local consumption. We further note significant premiums being paid in international markets for washing, certification, vertical integration, and origin’s geographical indications. The latter two are especially rewarding in emerging high-end markets.

There have been significant domestic policy reforms in the last decade in Ethiopia that affected the structure and performance of the coffee export sector. From December 2008 onwards, it became mandatory for private traders to sell their coffee through the Ethiopian Commodity Exchange (ECX), a new modern commodity exchange. ECX trades standard coffee contracts based on a warehouse receipt system, with standard parameters for coffee grades, transaction size, payment, and delivery. The first level of quality control is decentralized and undertaken in nine liquoring and inspection units in major production areas. The establishment of the ECX has led to critical changes in the coffee value chain (Gabre-Madhin, 2012). Secondly, the government intervened in the coffee market on several occasions to reduce hoarding by exporters. In April 2009, six large traders were banned from exporting coffee summed excessive hoarding. The government revoked their licenses, closed down their warehouses, seized their coffee stocks, and sold them on their behalf (Alemu, 2009). A policy was further implemented in May 2011 that limited the amount of coffee an exporter can store. Failing to adhere to these regulations has led to banning coffee exporters, as seen in 2011 and 2013 (Araya, 2011).

Thirdly, there have been several changes regarding export taxes on coffee over time. Core changes include the removal of entry barriers (Proclamation No. 70/1993); the consolidation of all taxes and duties levied on coffee export into a single tax family (Proclamation No. 99/1998), which consolidated all taxes on coffee export to 6.5 percent; and, following the 2002 international coffee crisis, the waiving of all export taxes on coffee exports.

Finally, an Ethiopian Fine Coffee Trademark Licensing Institute was set up in February 2005 to set up a system to secure legal ownership in international markets of specialty coffee names (especially Sidamo, Harar, and Yirgacheffe). There was an original confrontation against this initiative, but they were ultimately settled. The goal of this effort was to add brand value to Ethiopian coffee.

To obtain better production, supply chain bottlenecks and poor productivity issues will need to be discussed. For illustration, if the producers had entry to increased seed, good tree control, and irrigation schemes in states where irrigation is available, they would see significant production improvements. Ethiopia’s coffee sector would advance from increasing social and individual sector partnerships geared toward increasing modernization and work speed. As elsewhere globally, the COVID-19 pandemic will have overarching effects on health, the economy, and security in Ethiopia and its export markets. On the other hand, profitable farms, which make up about five percent of total coffee Farms, are encountering frustrations in hiring laborers because of current travel restrictions. Moreover, the coffee farmers have to compete against the production of khat (Catha edulis), a bushy plant with stimulant properties, because of its: improved ability to withstand drought, infections, and pests; rapid improvement, assigning it to be harvested up to three times a year in areas with good water availability; and higher sales prices than coffee.

Therefore, we recommend the Ethiopian coffee export companies to:

- Diversify the product portfolio. In addition to primary agricultural products export, more attention should be given to fully and better processed and value-added manufactured items, improving the level of foreign currency policy reserves and facilitating import substitution.

- Make Ethiopian coffee export products competitive globally, special attention should be given to the policy of quality through better production methods, innovative packaging and storage, and strong supply chain management.

- Improve their management policy by hiring skilled professionals and managers, conducting export market research, and organizing themselves in associations. They should also take advantage of the opportunities created by regional economic integration agreements. Besides, Ethiopian exporters should make a portfolio analysis to choose which products, export, export, and exploit a favorable geographical location near Europe, Asia, and the Middle East.

- Improve the performance policy; for example, the Ethiopian Customs Authority should assign skilled personnel and cut its lengthy procedures to reduce delays. Besides, export-processing parties should be networked to improve efficiency and coordination. The Ethiopian coffee export promotion department should provide updated information to the business society and awareness creation about new international trade rules and regulations.

Author: Fuad Usmael Yusuf

References

Alemu, H. (2009). Through the grinds. Fortune, Edition, 06/21/2009. Online: http://www.addisfor-

tune.com/vol%2010%20no%20476%20archive/Through%20the%20Grinds.htm

Annual report. (2021). Commercial bank of Ethiopia. Online: https://nbebank.com/wp-content/uploads/pdf/annualbulletin/Annual%20Report%202019-2020.pdf

Araya, E. (2011). Ethiopia: Trade Ministry bans 16 coffee exporters from exchange floor, Addis Fortune, November 21st, 2011. Online: http://allafrica.com/stories/201111240122.html

Ayele, K. (2006). The Ethiopian economy: principles and practices. Ethiopia, Addis Ababa: Commercial Printing Enterprise.

Berhanu, L. (2005). Determinants of Ethiopia’s Export Performance: An econometric Investigation. In Alemayehu, S. et.al. Ethiopian Economic Association (EEA). Proceedings of the Second International Conference on the Ethiopian Economy. Addis Ababa, Ethiopia: EEA.

Daviron, B., Ponte, S. (2005). The Coffee Paradox, Global Markets, Commodity Trade and the Elusive Promise of Development. Zed Books, London, New York.

Dwivedi, D N. (2002). Managerial Economics. Sixth Revised Edition. New Delhi: Vikas Publishing House Pvt. Ltd.

Gabre-Madhin, E. Z. (2012). A market for Abdu: Creating a Commodity Exchange in Ethiopia. Occasional Essays Series. Washington, DC: International Food Policy Research Institute (IFPRI).

Green Coffee Production by Country in 1000 60 KG BAGS. (2021). Index Mundi. Online: https://www.indexmundi.com/agriculture/?commodity=green-coffee&graph=production

Hill, C. W. (1998). Global Business Today. USA: McGraw-Hill Companies.

International Coffee Organization (ICO). (2013). Online: http://www.ico.org/new_historical.asp

Jeannet, J. P. & Hennessey, H. D. (2001). Global Marketing Strategies. 2nd ed. Mumbai: Jaico Publishing House.

LMC. (2003). Review of the Ethiopian Coffee Market. Report prepared for DFID, Programme of Advisory Support Services for Rural Livelihoods. LMC International Ltd, Oxford.

Pendergrast, M. (2010). Uncommon grounds: The history of coffee and how it transformed our world, Basic Books, New York, 424p.

Ponte, S. (2002). “The ‘Latte Revolution’? Regulation, Markets and Consumption in the Global Coffee Chain”. World Development, 30(7): 1099-1122

Teuber, R., Herrmann, R. (2012). “Towards a differentiated modeling of origin effects in hedonic analysis: An application to auction prices of specialty coffee”. Food Policy, 37: 732-740

New Horizons in Education and Personal Development

New Horizons in Education and Personal Development

LIGS University and ICAN Open Doors to Long-Term Success In today's dynamic…

Relationship Management in the Oil and Gas Organizations: The Niger Delta Experience

Relationship Management in the Oil and Gas Organizations: The Niger Delta Experience

No organization anywhere in the world could derive sustainable development without imbibing…

How to write in academic style | APA 101

How to write in academic style | APA 101

Writing an academic paper can be rough. There are so many rules…