The Finance Function: A Framework for Analysis by ICAEW – A thorough review and implications for digital transformation

The report, titled The Finance Function: A Framework for Analysis, is a study conducted by the Finance & Management Faculty of the ICAEW (2011) that offers an in-depth examination of the finance function within organizations. ICAEW stands for the Institute of Chartered Accountants in England and Wales. It is a professional membership organization based in the United Kingdom that represents chartered accountants and promotes the highest standards of accounting and financial reporting. The ICAEW is one of the world’s leading professional bodies for accountants and finance professionals. The report is structured with a detailed framework, which analyzes the many aspects of financial activities and what shapes their implementation. The publication includes insights, analyses, and practical implications, making the report a valuable resource for finance professionals, organizational leaders, and scholars.

This review paper will go through each chapter of the report and capture the essence and implications of every section including major shortcomings. In the conclusion part of this review paper, we will delve into the report’s practical implications particularly for digital transformation.

Background

Corporate finance is grounded in a variety of theoretical frameworks that explain the complex responsibilities and challenges encountered by firms. Frameworks in corporate finance provide critical insights into the responsibilities and challenges faced by firms, guiding decision-making processes and strategic financial planning.

Jaworski in May 2011 published a paper in which he elaborates the main components and tasks in corporate finance and identified three main parts:

- Capital budgeting

- Working capital management

- Financial structure

Additionally, Jaworski also highlighted the main problems and challenges arising from these areas particularly from working capital management including asset maintenance costs, cash management, credit limit etc. It should be noted that Jaworski’s paper only provides limited insights into finance responsibilities and challenges and does not further elaborate on topics such as compliance, controlling or risk management.

Therefore, the Finance and Management Faculty of the ICAEW created a more sophisticated theoretical model to aid managers in analyzing the financial functions and the distinctive contexts in which they operate. This model was developed from insightful dialogues with finance professionals, a rigorous review of existing literature, and the ICAEW’s own expertise. The framework aspires to establish a unified language and an agenda to facilitate discussions about the finance function and its associated departments.

Structure of the report

The whole report is structured into seven chapters:

- Chapter one (Overview) provides an overview of the report as well as implications and next steps. It also provides a graph which summarizes the entire framework which consists of:

- Financial activities

- Interrelations between the activities

- External drivers

- Chapter two (The nature and content of finance activities) identifies the main financial activities based mainly on literature review.

- Chapter three (The interactions between finance activities) delves into the interrelationships between the activities identified in chapter two.

- Chapter four (Inherent tensions and challenges) identifies the main challenges of financial activities mainly based on literature review. These challenges are connected to the main framework.

- Chapter five (The role of the finance department) provides an in-depth analysis of the finance department and its activities based on chapter two. It also identifies the importance and the amount of efforts of each activity. The chapter provides important inspiration for digital transformation in finance.

- Chapter six (Drivers shaping the implementation of finance activities) names the main external drivers (Environment, Accounting, Organization) and their impact on corporate finance.

- Appendix 2 informs the reader about the research methodology to gather the results of this report.

In our review paper, we will go through each of the chapters and interpret the results.

The Framework

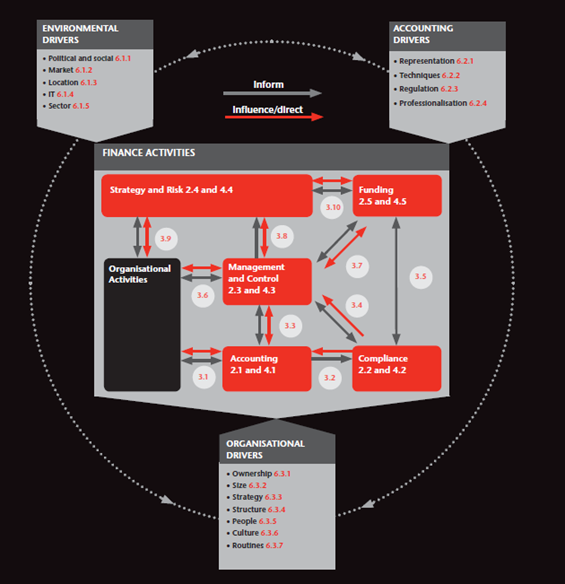

Here, the authors present the summary of the core framework that anchors the entire report. The results are based on literature review and surveys with CFOs and encapsulate the diverse elements, dynamics, and drivers of finance activities, offering readers a holistic view of the finance function’s ecosystem.

Source: Screenshot from The Finance Function: A Framework for Analysis, ICAEW (2011), page 3

The model consists of two main elements:

Finance Activities

In this sub-section, the authors provide insights of finance activities based on the main activities from the framework (Accounting, Compliance, Management and Control, Strategy and risk, funding), exploring their purposes, interactions, information content, operational dynamics, and inherent challenges. It offers a balanced view of the theory and practical implications that characterize finance functions. Moreover, it provides a list of challenges of each main activity which can be of high value for organizations. Therefore, the way organizations deal with these challenges will have significant impact on the organization’s efficiency.

The Drivers that Shape Finance Activities

The authors explore the environmental, accounting, and organizational drivers that influence finance activities, giving the reader a first introduction into the external factors. Readers are therefore prepared for a detailed analysis of these drivers in the later stage of the study.

Practical Implications

In the final part of the overview, the authors offer straightforward advice based on the framework, stressing the need to regularly look at the bigger picture and balance well-made plans with the ability to change as needed. Here’s a simpler breakdown of the main points:

- Keep the Big Picture in Mind: Always remember the overall goals and objectives. It’s easy to get lost in the details, so regularly take a step back to ensure you’re still on the right path.

- Question ‘Best Practices’: Be cautious with so-called ‘best practices’. They might not always be the best fit for every company. Always consider your specific situation and needs.

- Balance Planning with Flexibility: It’s essential to have a plan but equally important to be able to adapt to unexpected changes. The business world can change fast, so stay flexible.

- Stay Realistic: Be honest about what’s achievable. Set realistic goals and expectations to ensure success and avoid unnecessary disappointments.

- Focus on Ethics and Resilience: Stick to ethical practices and build a resilient business. It helps in navigating challenges and ensures the company’s longevity and good reputation.

In short, it’s about keeping an eye on your overall goals, being careful with applying general ‘best practices’, balancing detailed plans with the ability to adapt, staying realistic in your expectations, and maintaining ethical and resilient business practices in the field of corporate finance.

Next steps

In this final section, the authors offer additional steps to take after reviewing the framework, aiming to further its understanding and application:

- Discussion and Interpretation: The first step involves engaging in conversations to better understand and apply the framework. Talking about it with others can lead to new insights and a more in-depth understanding.

- Review and Organize Existing Knowledge: Reflect on what you already know and try to organize this information within the context of the new framework. This helps in seeing where existing knowledge fits and where gaps might exist.

- Expand the Framework: Consider how the framework can be developed further. This could involve more research to refine and expand its concepts, ensuring it remains relevant and useful.

The framework stands as a strong starting point for more research in corporate finance. For example, it can help identify key challenges in the field, using the activities outlined in the framework as a guide. Additionally, digital transformation is a key focus, and this framework can support efforts in this area as well. It offers a theoretical foundation to base digitalization initiatives on, helping businesses navigate the shift to more digital operations.

In simpler terms, after studying the framework, it’s helpful to talk about it with others, think about how existing knowledge fits into it, and consider ways to improve and build upon it. It’s a useful tool for addressing current challenges in finance and can support businesses as they move towards more digital ways of working.

Conclusion

The “OVERVIEW” section of the report is a comprehensive introduction, offering detailed insights into the finance function’s diverse nature. It provides the theory fundamentals and prepares the reader for the in-depth analyses and discussions that follow in the next sections of the report. Additionally, it is remarkable that the authors discussed the practical implications and the next steps for this research in the first chapter in order to provide clarity, to engage readers immediately by highlighting real-world relevance, and to attract support and collaborations by outlining the research’s significance and future directions.

The nature and content of finance activities

This section is a core component of the report, presenting a detailed model that describes the main elements and activities of finance activities within organizations. This section additionally identifies the relationships between various finance activities, offering a comprehensive perspective that connects theory and practice. To ensure full transparency, the report includes a list of surveys from which the results were identified.

Finance Activities

The report categorically outlines the core finance activities, including strategy and risk, funding, management and control, accounting, and compliance. Each activity is explored in detail, with insights into their operational dynamics, challenges, and opportunities. Additionally, the chapter also includes a list of surveys from which the results were identified to increase transparency. According to the framework, main finance functions within an organization can be grouped in to 5 categories:

- Accounting

- Compliance

- Management and control

- Strategy and risk

- Funding

Accounting

Accounting is defined as “recording financial consequences of organizational activities” according to ICAEW (2011). It measures the results of an organization’s economic activities and conveys this information to a variety of stakeholders, including investors, creditors, management, and regulators. Based on the report by ICAEW, accounting consists of three main functions:

- Transaction processing which records and settles all financial transactions within an organization.

- Reporting which aggregates all transaction information and consolidates them into financial reports for both internal and external stakeholders.

- Financial control which ensures that all transactions are correctly recorded.

Compliance

The main purpose of compliance is to meet the policies and requirements of governmental and regulatory bodies and consists of two elements:

- Regulatory requirements which enforce certain governance and control standards within an organization.

- Tax requirements which enforce tax compliance in accordance with national authority.

Management and control

According to ICAEW, Management and Control is to utilize financial support information to “inform, monitor and instigate operational actions to meet organizational objectives”. This definition is in-line with the financial business partner role in many companies. Management and Control usually consists of below responsibilities:

- Financial processes, which are based on the organizational policy.

- Applications, which focuses on how information is aggregated and analyzed to support corporate decision-making.

- Internal auditing, which ensures that financial control mechanisms are working as expected.

- Management accounting, which is described as “distinguishing, examining, deciphering and imparting data to supervisors to help accomplish business goals.”

Strategy and risk

In the context of corporate finance, strategy refers to the long-term plan of action adopted by a company to achieve its goals and objectives. It involves making decisions about resource allocation, competitive positioning, and value creation to maximize shareholder value. A corporate finance strategy includes various aspects, such as capital structure, investment decisions, mergers and acquisitions, dividend policies, and risk management.

Funding

Funding refers to the provision of financial resources, typically in the form of capital or money, to support a specific project, organization, or individual. It involves obtaining the necessary funds to meet financial requirements and enable the implementation of planned initiatives. In the context of corporate finance, funding usually refers to the process of acquiring capital to finance a company’s operations, investments, and growth. This can be achieved through various means:

- Equity financing incl. issuing shares or ownership stakes in the company.

- Debt financing incl. borrowing money through loans or issuing bonds.

- Alternative financing methods incl. crowdfunding, venture capital, private equity.

Conclusion

This section offers readers a panoramic view of the finance function, integrating diverse activities into a model that promotes understanding, analysis, and optimization. The main goal of the section is to present the most important activities of corporate finance summarized into five sub-categories.

The interactions between finance activities

In this chapter, the authors describe the interactions between various finance activities identified from chapter two. The authors distinguish between two types of interactions:

- Inform: Information from one activity to be used by another.

- Influence and Direct: One activity decides and influences how other activities are carried out and implemented.

For details, please refer to graph 1 in chapter 1 of this paper.

Conclusion

The main benefit of identifying interactions is to emphasize the interrelations between certain activities. Instead of simply listing important activities, the authors pay high attention on interactions to help readers understand that financial activities are connected rather than isolated.

One potential area for further study is exploring the resilience and adaptability of these interconnected financial activities in the face of external shocks, such as economic downturns. How do these interactions mitigate the impacts of such shocks? Understanding this can help to create a more robust financial system capable of tackling challenges.

Another ground for investigation is in technological integration within finance. As digital transformation continues to benefit every part of financial activities, understanding how technology influences and is influenced by these interactions will be important. This could lead to the development of advanced tools and platforms that empower these interactions for better efficiency and security in finance.

Inherent tensions and challenges

Finance functions relate to tensions and challenges. The report offers an in-depth analysis of these challenges that is both informative and pragmatic based on extensive literature review. The identified challenges are all linked to the previous finance activities and interrelations based on the framework:

- Challenges related to Accounting.

- Challenges related to Compliance.

- Challenges related to Management and Control.

- Challenges related to Strategy and Risk.

- Challenges related to Funding.

Please refer to the report for a detailed overview of all challenges.

Conclusion

The outlined challenges are integral to understanding the nature of the finance functions and their corresponding tensions, the interrelations between financial activities add layers of complexity but also offer new opportunities.

Future research and practice should focus on developing adaptive solutions that solve these challenges. Cross-functional collaborations, technological innovations, and policy reforms will be important to navigate the complexities and challenges for transformation in finance. Each challenge, when addressed with foresight and innovation, has the potential to further improve the finance sector. Therefore, this section can serve as a foundation for solutions related particularly to digital transformation.

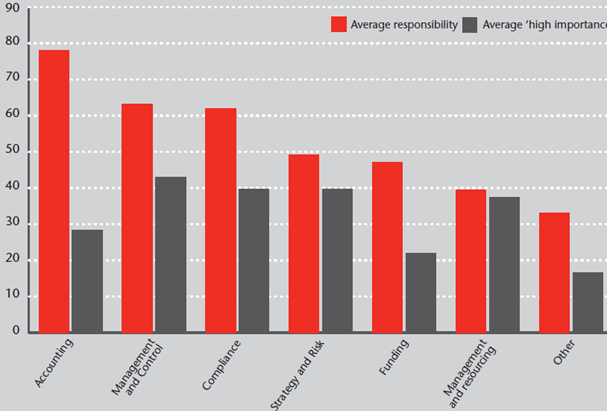

The role of the finance department

In this chapter, the authors of the report investigate both the amount of responsibility as well as the importance of each of the five main areas of corporate finance and its sub-activities. The results are based on surveys and interviews and therefore need to be interpreted with caution. However, some important patterns do emerge and provide important insights for further research.

Source: Screenshot from The Finance Function: A Framework for Analysis, ICAEW (2011), page 43

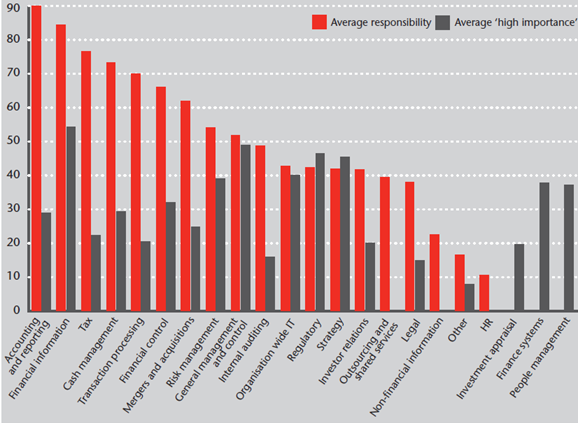

From the above graph, we can see that although Accounting requires the highest amount of responsibility and effort, its importance is only limited. Another graph including the sub-activities presents similar results:

Source: Screenshot from The Finance Function: A Framework for Analysis, ICAEW (2011), page 44

Again, we can see that repetitive tasks such as accounting, reporting and transaction processing require large amount of efforts and responsibilities while the importance rating is rather medium. Tasks with lower responsibility such as strategy and general management have ‘high’ importance rating. The authors emphasize that results should be interpreted with caution as they are based on averages of surveys. On the other hand, the total number of surveys is high which establishes a solid data foundation.

Conclusion

In recent years, digital transformation has become one of the hottest topics within organizations as it helps the organization to focus more on the business rather than on repetitive tasks. People will spend less time on preparing reports and more time on analyzing important business insights from real-time data empowering them to make better strategic decisions. A Deloitte survey from 2018 predicts that “new service delivery models will emerge as robots and algorithms join a more diverse finance workforce” in the coming years. According to another report by KPMG (2021), RPA can lead to:

- Increased operational visibility.

- Stronger data security.

- Reduction in cost.

- Improved compliance.

- Optimized efficiency and better service.

These benefits are undoubtedly crucial for any organization’s digital transformation journey. However, to deeply understand the RPA benefits, it is equally important to identify the main responsibilities of the finance department within an organization to acquire a solid theoretical foundation.

The survey results from the current report strongly suggest that digital transformation can considerably help to reduce the finance team’s efforts in repetitive tasks such as accounting and transaction processing and therefore lays the foundation for in-depth research to drive digital transformation of corporate finance.

Drivers shaping finance activities

In this chapter, the authors discuss how external factors influence financial decision-making and activities within organizations. The external factors consist of:

- Environmental drivers: Provide context within the organization and influence how decisions are made e.g., political and social drivers.

- Accounting drivers: Impact corporate finance directly and indirectly e.g., techniques and regulations.

- Organizational drivers: Influenced by both environmental and accounting drivers e.g., ownership, size, culture etc.

The authors list all external drivers one-by-one and provide detailed information on each of the driver. The identification of these drivers is based on extensive literature review from papers of the past 50 years.

Conclusion

The roles of environmental, accounting, and organizational drivers are crucial in making smart financial decisions within companies. Environmental drivers are influenced by the world around us, including politics and society. They set the scene for how companies make choices. Accounting drivers are the rules and methods that companies must follow when dealing with money. Organizational drivers, like the company’s size and culture, are shaped by both environmental and accounting factors. An organization may have efficient tools and processes, however, if the organization culture is toxic and unreasonable, financial activities will be negatively impacted. It is highly appreciated that the authors of this framework do not ignore external factors that might influence decision-making and activities within a company.

In short, these external factors together create a guide for making financial decisions that are not only rule-compliant but also fit well with the company’s specific needs and the world around it. Each factor ensures that financial planning is complete, flexible, and ready for any challenges that might come its way.

Research methodology

In appendix 2 of the study, we learn that the research approach of the report is divided into three parts:

- Extensive literature review of academic and practitioner studies to obtain a solid theory foundation.

- Synthesizing and interpreting the study findings and develop a new proposal.

- Consultation with experts through interviews, leading to introduction of new proposals.

The literature review is based on 261 studies while the focus lies on 20 surveys involving CFOs or finance executives. These papers provided relevant evidence about financial activities and how they are implemented. Afterwards, the authors collected the most important activities and drivers and consolidated them into the framework. The model of the framework was developed based on iterations, discussions, and consultations. Finally, the draft of the framework was consulted with leading practitioners and academics and the feedback resulted in further improvements of the framework.

Nonetheless, the study has several limitations:

- Many studies were produced by commercial organizations. Bias is possible as these organizations are interested in reaching certain business goals.

- The findings of the study are mainly literature-based. While the results have been consulted with practitioners and academics, both qualitative and quantitative research is limited for this report.

- The results of the study need to be further confirmed based on quantitative methods.

- Sample Size and Diversity: The focus on 20 surveys involving CFOs or finance executives might not be sufficiently representative. A broader sample of respondents including mid-level finance professionals and those from diverse industries can offer a more comprehensive insight.

- Geographical Limitations: The framework may not fully consider the regional and cultural variations in financial practices and regulations as only English literature was reviewed. Different regions may have unique financial management approaches, regulatory environments, and business cultures.

- Technology and Innovation: The rapid pace of technological innovation and digital transformation is not sufficiently captured. Technology plays a significant role in modern financial management, impacting everything from data analytics to cybersecurity.

- Implementation Challenges: The practicality of implementing the proposed financial framework in real business settings is not clearly investigated. Potential operational and logistical challenges, resource constraints, and resistance to change can affect the framework’s efficiency.

- Time Sensitivity: The findings and proposals might become outdated quickly given the dynamic nature of the global business environment. Continuous updates will be necessary to keep the framework relevant.

Conclusion

This report provides a comprehensive summary of finance functions within organizations. It provides a detailed framework that examines various aspects of financial activities and the factors defining their implementation. The practical implications and next steps presented in this report make it a valuable resource for finance professionals, organizational leaders, and scholars.

While the report provides a solid theoretical foundation and offers practical recommendations, it is important to identify its limitations, including potential biases in the sources, the need for further quantitative research, and the importance of considering regional and technological variations. Nonetheless, this report serves as a valuable basis for those seeking to deep-dive into corporate finance and the opportunities generated by digital transformation.

Furthermore, the report’s insights extend to how it can benefit digital transformation efforts within the finance sector. Here’s how:

- Strategic Foundation: The report’s framework serves as a strategic cornerstone for organizations initiating on digital transformation. By comprehending the core finance activities and their interactions, companies can pinpoint areas where digital solutions can increase efficiency, streamline operations, and enhance decision-making.

- Identifying Efficiency Gaps: As highlighted in the report, specific finance activities, such as accounting and transaction processing, involve labor-intensive, repetitive tasks. Digital transformation initiatives can empower automation technologies like robotic process automation (RPA) to significantly reduce manual workloads. This not only liberates human resources but also mitigates the risk of errors.

- Data-Driven Insights: Digital transformation often revolves around data-centric decision-making. The report underscores the significance of management and control, which utilizes financial data to guide operations. Armed with the right digital tools and analytics capabilities, organizations can obtain deeper insights from their financial data, enabling more informed and strategic decision-making.

- Enhancing Compliance: Compliance stands as a critical factor of finance, and it’s an area where digital transformation can have considerable influence. Automation and data-driven solutions can aid organizations in adhering to new regulations, reducing the likelihood of non-compliance and associated penalties.

- Efficiency and Cost Savings: Digital transformation initiatives, when aligned with insights from this report, can result in improved operational efficiency and cost savings. Through the optimization of finance activities, organizations can allocate resources more efficiently, reduce overhead, and enhance financial performance.

- Cybersecurity and Data Protection: With more and more digital technologies, cybersecurity is of crucial importance. The report’s focus on control mechanisms and compliance emphasizes the need for robust cybersecurity measures to protect sensitive financial data.

Bibliography:

Finance and Management Faculty ICAEW., (2011). The Finance Function: A Framework for Analysis. Finance Direction Initiative.

Deloitte., (2018). The robots are waiting – Are you ready to reap the benefits?

KPMG., (2021). Digital Transformation of finance function using RPA.

Gartner., (2021). The Digital Future of Finance. Gartner for Finance.

Gartner., (2019). White Paper – Revolutionizing via Robotics: Hear from a Peer.

Author: Mingzhe Li, student LIGS University

Approved by & Co-author: Prof. Grigory Sergeenko, lecturer LIGS University

Employee Experience Outcomes of First-Line Leadership Implementation of Strengths-Based Leadership and Coaching, guided by StrengthsFinder 2.0

Employee Experience Outcomes of First-Line Leadership Implementation of Strengths-Based Leadership and Coaching, guided by StrengthsFinder 2.0

Short annotation: This study explores the influence of strengths-based leadership, as practiced…

New Horizons in Education and Personal Development

New Horizons in Education and Personal Development

LIGS University and ICAN Open Doors to Long-Term Success In today's dynamic…